Scopes of Emissions

What are Scope 1, 2, and 3 Emissions?

What are Scope 1, 2, and 3 Emissions?

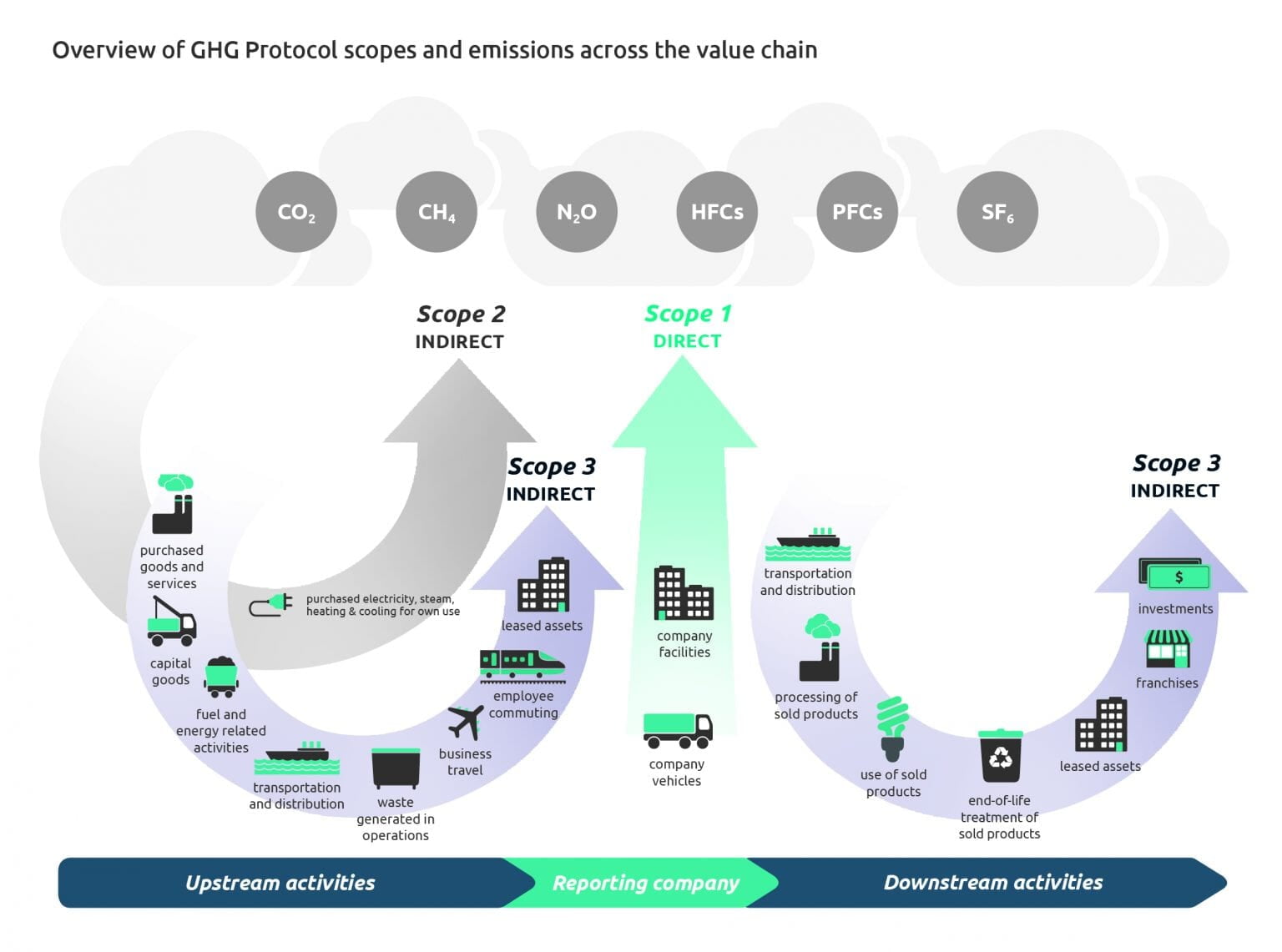

When it comes to measuring and reporting greenhouse gas emissions, it is important to distinguish between different sources and activities that contribute to the global warming potential. The Greenhouse Gas Protocol, the most widely used international accounting tool for government and business leaders to understand, quantify, and manage greenhouse gas emissions, defines three scopes of emissions:

Scope 1

Scope 1 emissions are direct emissions from owned or controlled sources. These include emissions from combustion in boilers, furnaces, vehicles, and other equipment; emissions from chemical production, processing, and use; and emissions from physical or biological processes such as respiration and fermentation.

Scope 2

Scope 2 emissions are indirect emissions from the generation of purchased energy. These include emissions from electricity, heat, steam, or cooling that are consumed by the reporting entity but generated by another entity. For example, if a company buys electricity from a power plant that burns coal, the emissions from the coal combustion are scope 2 emissions for the company.

Scope 3

Scope 3 emissions are all indirect emissions (not included in scope 2) that occur in the value chain of the reporting entity, including both upstream and downstream emissions. These include emissions from the extraction and production of purchased materials and fuels; emissions from transportation and distribution of purchased goods and services; emissions from the use and disposal of products and services; and emissions from leased assets, franchises, and investments.